|

We’ve all heard the story: a low-income individual builds a successful business thanks to micro-loans, creating employment for many and improving their living conditions in doing so. Many micro-lending companies of all types, especially mobile-based ones, have emerged in recent years (The Conversation, 2019). They claim financial inclusion as the best way to achieve long-term impact, as was the case for Agness Mpinganjira - an example of many. Being a mother of four, Agness was struggling to financially support her children through her milk business. Using her microloan, Agness was able to expand her business and begin selling scones, increasing her weekly income fivefold, from £1.05 to as much as £5.20. In the end, the microloan allowed Agness to pay entirely for her children’s education (Microloan Foundation, 2019). While this story may be inspiring, it is not always reflective of the reality of individuals in Sub-Saharan countries.

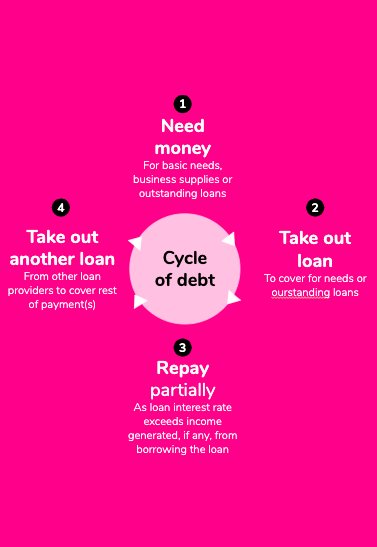

Micro-lending has, in recent years, increased financial inclusion through greater access to capital - in 2014, approximately 80% of Kenyans aged 15 and over have taken out a loan, compared to 56% in the United States (The Economist, 2018). Such financial “inclusion” does come at a cost: aside from significant debt, certain individuals find themselves facing increased anxiety, due to working longer hours. Others reduce already thin food budgets to be able to make repayments. Some even find themselves victims of aggressive debt collectors, who seize personal possessions, publicly shame or even imprison debtors with late repayments. In other words, access to capital is not always synonymous with prosperity. … To the Cycle of Prosperity If we’re serious about helping individuals in developing countries achieve lasting growth, then this cycle must be inverted. What if loans were used for sustainable income-generating activities with potential for long-term growth, as was the case for Agness? Or what if interest rates were lower so that individuals could easily repay their loan entirely, without taking on more debt? Currently, small and medium enterprises (SME) struggle converting jobs into wealth creation: in Kenya, while they contribute to 80% of job creation, they only account for 35% of GDP. In comparison, US SMEs generate the same GDP contribution with only 60% of jobs (Viffa Consult, 2018). In other words, SMEs in Sub-Saharan countries expand rapidly, but are unable to generate significant revenue. If loans were affordable and used towards business growth, formal employment would increase, along with good salaries, improved living conditions and higher purchasing power: that’s the cycle of prosperity. What must be done to achieve this change? Creating a balance between the repayment rate and growth production is a good start. Many microlending companies claim to have loan repayment rates ranging from 95 to 99%, but how many of these loans achieve lasting social and economic benefits? While ensuring loans get repaid is important, as loans can be recycled to benefit many, focusing solely on repayment rate disconnects us from microlending’s ultimate objective: improving living conditions through financial inclusion. While microlending is a start, we can learn from the last decade and make the adjustments necessary to truly help individuals and businesses in need.

1 Comment

7/26/2022 11:44:00 am

Hey, Leave a Reply. |

|

Become a Mentor

Mkono Mentors are young professionals willing to share their insights with entrepreneurs. And learn from them in the process. Contact us

community@mkono.org |

Get Involved

Interested in contributing? Mkono might have the volunteer opportunities you're looking for. |

Subscribe to keep up to date

|

Copyright © 2020