|

This article is part of Mkono's new Mawazo thought leadership series. At Mkono, we want to continually share insights on the ever-changing landscape of microfinance, SME growth, economic development and more. Microcredit Organizations and Microfinance Institutions (MFIs) have existed in Kenya since the 1990s as a means to provide financial support to Small and Medium Enterprises (SMEs). SMEs face several challenges in accessing loans from banks and other traditional financial institutions, often influencing their decision to work with MFIs instead. Entrepreneurs working with Mkono have listed a few of these challenges which have included the size and type of their enterprise, high interest rates charged by formal banks, greater risk associated with formal bank loans as well as the bureaucracy that exists in formal institutions, which leads to lengthy and tedious loan processes.

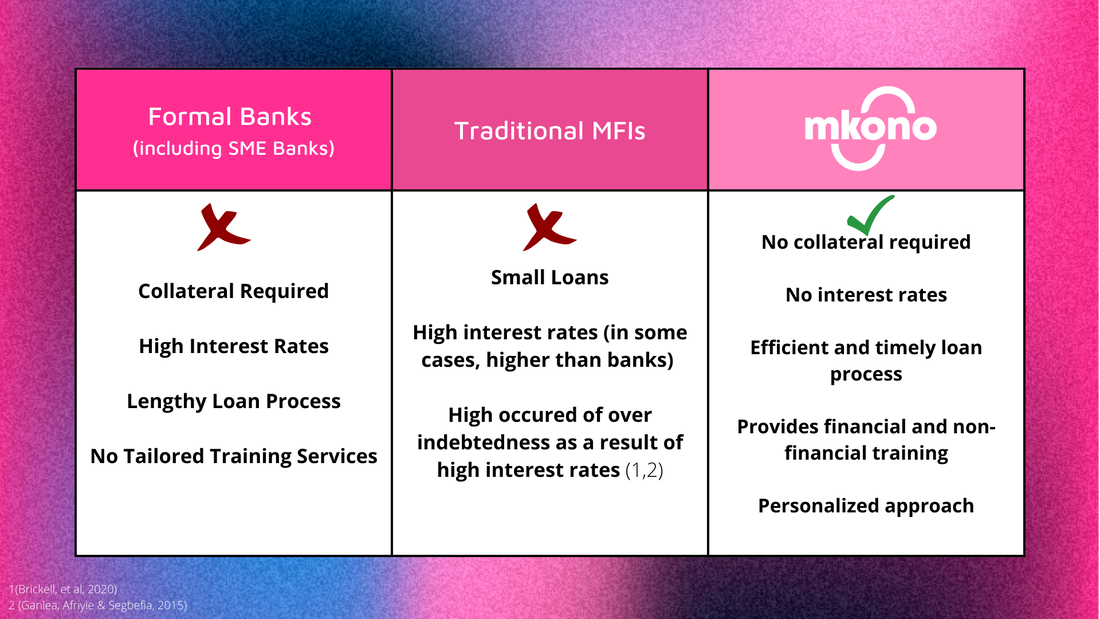

Traditional MFIs Come with Challenges MFIs have spread widely over the years as an alternative to formal bank loans, specifically in low-income nations. MFIs are however continually criticized for their for-profit motives and high interest rates(Elahi & Rahman, 2006). Interest rates are traditionally used as the main source of funding for MFIs; unfortunately high interest rates can have detrimental physical and mental effects on debtors who are unable to pay their loans. For example, debtors may be shamed in their communities for defaulting on a payment, causing a significant amount of stress (Karim, 2012). In other instances, studies have shown that women will sacrifice their physiological needs such as food and sleep, in order to increase household income and pay off their loans (Brickell, et al., 2020). With the several challenges and obstacles entrepreneurs face when trying to finance their enterprises through traditional MFIs and financial institutions, it is important to consider alternative sources of funding for continued SME growth. Kenya’s 2022 GDP growth rate is projected at 5.9 %, with SMEs contributing to 24% of overall GDP; SMEs drive over 90% of private sector business and make up 93% of the total labour force (FSD Kenya, 2021). Organizations such as Mkono play an integral role in economic growth as they provide an essential service to communities traditionally overseen by the formal financial sector. Nairobits and Mkono Partnership “We have a number of SME banks… they are able to provide credit but their interest rates are a bit too exorbitant. We call these expensive credit facilities.” - Nairobits representative An interview with Nairobits highlighted key issues that young entrepreneurs face when trying to access credit in Kenya. These issues included extremely high interest rates as well as a lack of supportive policies catered to young entrepreneurs. This remains an issue as they continue to be excluded from the financial industry, ultimately inhibiting SME growth. Moreover, Covid-19 significantly limited entrepreneurs’ movements and productivity, adding to the existing hurdles SMEs face. A Nairobits representative stated that; “One of the significant challenges we saw was the restriction of movements which limited people’s capacity to sell themselves or to sell their ideas.”- Nairobits representative Nairobits emphasized the importance of acknowledging that entrepreneurs have unique needs and interests which go beyond financial needs. Through its various community partnerships, including the one with Nairobits, Mkono seeks to provide entrepreneurs with resources beyond financial means to support SME growth in Kenya. Formal Banks, Traditional MFIs and Mkono Table 1 below provides an overview of the challenges entrepreneurs have faced in accessing finance to support their SME, and how Mkono addresses these challenges.  Driving SME Growth in the Face of COVID-19 In 2020, Kenya’s economic growth was reported at -0.3% as a result of Covid-19, which was significantly lower than the previous year’s growth rate of 5.4% (World Bank Group, 2020). Entrepreneurs at all levels were negatively impacted, and the crisis made it increasingly difficult to access loans for business growth. Entrepreneurs working with Mkono stated that while traditional financial institutions could not support them during the pandemic, Mkono remained a reliable and ongoing source of funding. Founder of Tunga Tunga Hcrafts stated that working with Mkono was “like working with family” - Lornah Mukasa. She explains that in addition to providing interest free loans, Mkono made the entire process, from loan issuance to loan repayment “simple and stress free.” Mkono loans allowed entrepreneurs to continue to grow their enterprises during the pandemic. House of Asaa and Tunga Tunga Hcrafts experienced substantial growth from 2019-2021 with Mkono’s support. Founder of House of Asaa explained how Mkono’s loan supported his growth during this period; “I wanted to upgrade my gear, and my main tool of trade is my camera … it (Mkono’s loan) came at a very crucial time and I loved how it was interest free … and the payback timeline was quite friendly.” – Joseph Mbugua Tunga Tunga Hcrafts’ growth over the past two years includes an increased online presence as well as an increased employee base. Lornah stated that; “Mkono’s loan opened doors for me, allowing me to open doors for others.” – Lornah Mukasa Mkono continues to support entrepreneurs in achieving their long term business goals while also contributing to the Sustainable Development Goals (SDGs); specifically promoting sustained and inclusive economic growth (SDG8) and reduced inequality within and among countries (SDG10) (United Nations, n.d.). Works Cited

African Review. (2017, July 14). SMEs are Growing Kenya's Economy. Retrieved from African Review:https://www.africanreview.com/finance/business/smes-are-growing-kenya-s-economy-3#:~:text=Kenya's%202017%20overall%20GDP%20growth,3%20percent%20of%20the%20GDP. Brickell, K., Picchioni, F., Natarajan, N., Guermond, V., Parsons, L., Zanello, G., & Bateman, M. (2020). Compounding crises of social reproduction: Microfinance, over-indebtedness and the COVID-19 pandemic. World Development, 105087-105090. Elahi, K. Q.-I., & Rahman, M. L. (2006). Micro-Credit and Micro-Finance: Functional and Conceptual Differences. Development in Practice, 476-483. FSD Kenya. (2021, March 17). The Value of (in)formality: a case study of MSEs in the Nairobi CBD. Retrieved from FSD Kenya: https://www.fsdkenya.org/nairobi-mse-study/ Ganlea, J. K., Afriyie, K., & Segbefia, A. Y. (2015). Microcredit: Empowerment and Disempowerment of Rural Women in Ghana. World Development, 335-345. Karim, L. (2012). The Hidden Ways Microfinance Hurts Women. Retrieved from Brandeis Magazine: https://www.brandeis.edu/magazine/2012/fall-winter/inquiry/karim.html Rohregger, B., Bender, K., Kinyanjui, B., Schuring, E., Ikua, G., & Pouw, N. (2021). The Politics of Implementation: The Role of Traditional Authorities in Delivering Social Policies to Poor People in Kenya. Critical Social Policy, 404-425. Schicks, J. (2013). Over-Indebtedness in Microfinance – An Empirical Analysis of Related Factors on the Borrower Level. World Development , 301-324. United Nations. (n.d.). The 17 Goals. Retrieved from The United Nations: https://sdgs.un.org/goals World Bank Group. (2020, November 24). Kenya Economic Update, November 2020: Navigating the Pandemic. Retrieved from Open Knowledge Repository: https://openknowledge.worldbank.org/handle/10986/34819

0 Comments

Leave a Reply. |

|

Become a Mentor

Mkono Mentors are young professionals willing to share their expert insights with entrepreneurs. |

Become a Volunteer

Interested in making a difference? Mkono might have the fulfilling volunteer opportunities you're looking for. |

Subscribe to keep up to date

|

Copyright © Mkono 2024