Declan works in the investment space and has experience in the private, for-profit, nonprofit and government sectors. Today, he leads Afrinet Capital, a venture capital firm he co-founded that aims to connect investors in developed economies with entrepreneurs in Sub Saharan Countries. Being also an advisor for several start-ups, Declan works closely with entrepreneurs to help them secure funds for their businesses and build their working portfolios. He shared with us his experience and expert opinion on the topic. The Financing Options Available to Entrepreneurs Depending on the type of business, the funding options entrepreneurs have access to might vary largely. As Declan explains, "Tech [companies] --startups-- for example, have access to more progressive offerings of funding, such as angel investing and venture capital." However, in Kenya where 98% of all businesses are small and medium enterprises (SMEs) (International Trade Centre, 2018), most entrepreneurs, besides bootstrapping, turn to banks for grants and loans. Microlending and microfinance have also become popular alternatives to traditional banks, with over 600 available microlending platforms and a few dozen major microfinance organizations in the country alone. And lastly, the Kenyan government offers some funding opportunities for underrepresented groups, such as the Women Enterprise Fund and the Youth Enterprise Development Fund. Nevertheless, each option has its unique set of challenges.

The Challenges to Getting a Loan Securing a loan is not always easy for entrepreneurs. "Most banks require a large collateral," Declan explains, "And not everybody has enough collateral for a substantial amount of money." Combined with the need for a strong credit rating and the high-interest rates, traditional banks often are an unviable funding option for many small entrepreneurs. According to Declan, the lack of financial and business education represents an additional hurdle. In his experience, it is not uncommon to see entrepreneurs struggle with loan applications as it requires specific documentation that many are not familiar with, or even aware of. "The potency of the business, the proposals entrepreneurs have are not necessarily fundable," Declan mentions, "This becomes a problem when the way entrepreneurs market themselves does not make sense." But the most significant barrier Declan mentions is the limited funding sources. "There are financial facilities that cater to seed-level entrepreneurs. But even then, it is more competition-based than merit-based. So there are limited chances of securing that loan. Even if you get the loan, it might not be a sufficient amount to fund your business. [...] For example, micro-lending platforms, they don’t necessarily give funds you need, but funds they think you are able to pay back."

However, these products are not accessible to everybody. Similar to traditional banks, entrepreneurs must be able to prove their ability to repay the loan through either credit scoring, a business proposal and attendance to business training. Furthermore, the amount of credit offered is usually lower than traditional banks. Nonetheless, there is an added bonus : low interest rates. Ranging from 10% to 14%, they offer a competitive edge to commercial banks with usually higher rates. While the microfinance system in Kenya is not flawless, it is able to cater to a wider range of entrepreneurs from various income backgrounds with a level of flexibility higher than your everyday bank.

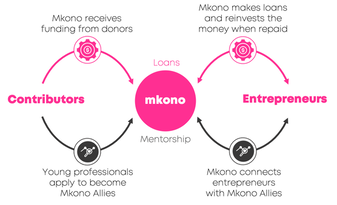

The Mkono Advantage

rates. Entrepreneurs can also expect to receive mentorship sessions from our network of professionals, our Mkono Allies. "What Mkono provides is really cool. The biggest problem is that there are limited resources. Mkono can help entrepreneurs gain knowledge and learn how to well invest their loans."

0 Comments

Leave a Reply. |

|

Become a Mentor

Mkono Mentors are young professionals willing to share their expert insights with entrepreneurs. |

Become a Volunteer

Interested in making a difference? Mkono might have the fulfilling volunteer opportunities you're looking for. |

Subscribe to keep up to date

|

Copyright © Mkono 2024